Markets still raw with supply risk

Full details

| Authors & editors | |

| Publisher | Milling & Grain |

| Year of publication | 2022 July |

| Languages | |

| Medium | Digital |

| Edition | 1 |

| Topics | |

| Tags | |

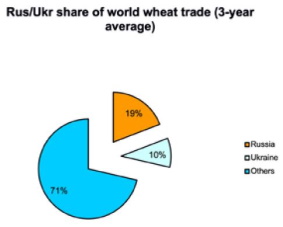

| Scope & content | ‘The market will take care of this” - wise words in the past month from Joe Glauber, former chief economist with the US Department of Agriculture, now senior research fellow at the International Food Policy Research Institute, Washington. Amidst all of the concern about global food shortages and rocketing costs, Mr Glauber’s address to a USDA webinar did not see agricultural markets as ‘broken,’ rather eventually encouraging enough output to rebuild supplies and restore calm. With plenty of incentive from high prices farmers will respond around the world – though, as Glauber noted, a key problem is timing. Two thirds of the wheat supply currently available to the world market was sown last autumn - before recent Ukrainian, Indian, US and European supply issues came to the fore. So, the big sowing response cannot come before latter 2022 and actual harvests not till mid-2023. This is why forward grain futures show little significant price moderation until July 2024 (maybe a little pessimistic?) It seems a long way off for milling and feed consumers facing rocketing input costs right now amid the backdrop of declining global stocks. Glauber compared things to the marketing years 2007-08 & 2010-11 when inventories were similarly tight & any bit of new information could be sending markets ‘screaming higher or lower.’ Still, in the end, “balance will be restored…the market will take care of this.” Global meal consumption – growth of which slowed almost to a standstill this season – is expected to increase in 2022/23 by about 3% but could expand more if prices – led by soya make a bigger retreat from this year’s record highs. Read more about: Two million tonnes is better than nothing Recent wheat news… Maize hopes pinned on US & LatAm crops Soya at decade highs Other oilmeals |

Pictures